Well, you have a few options.

So, you ask… what should I do with my money? Well, I think you have a few options. The one that’s right for you will depend on your circumstances, but I’ll try my best to cover them below.

1. Traditional savings accounts

Most of us have these, which are a compromise between accessibility, security, and interest. As a result, the interest rates of most savings accounts isn’t particularly high. Usually ranging from 1-4%.

Though interest rates here are relatively low whatever bank or building society you choose, it’s always worthwhile to compare deals using sites such as Martin Lewis’ Moneysaving Expert.

2. Long-term bond accounts

You basically agree to keep your money deposited for a certain period. Usually 1-5 years. Wellesley & Co are an example of a provider of bond accounts. Though I actually find the interest rates fairly disappointing when compared to some of the options I’ll mention further below.

3. Crowd-funding investment (aka. P2P lending)

FundingCircle.com is a good example of crowd-funding investment. You can also have a positive impact on UK small businesses – as your funding will go towards them.

With Funding Circle, the minimum amount to add to your account is £100, and the minimum to invest in each business is £20.

Funding Circle does extensive credit and background checks before accepting a business to be invested in.

Typically, you can expect interest rates of between 5-12% over the period of the investment, however since crowd-funding works as a bidding system, the exact rate will depend on how many people are prepared to invest in a specific business.

If you have a good spread between businesses, you shouldn’t be affected too much if one of the businesses defaults on the loan. If you’re getting worried or simple wish to get out early, simply sell your investments on their ‘loan parts’ marketplace.

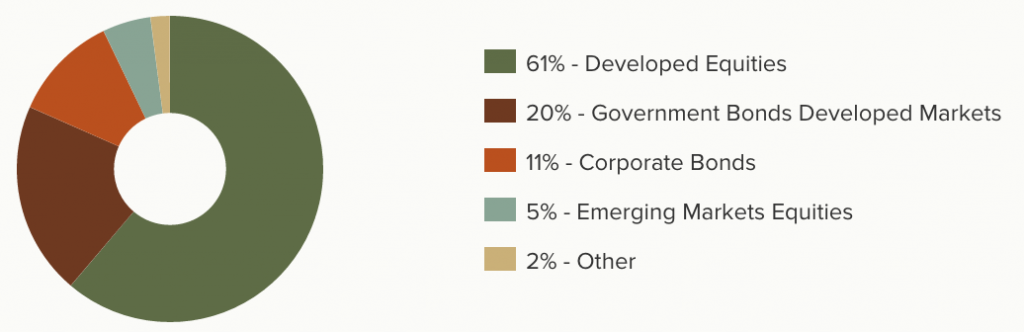

4. ‘Managed’ investment accounts

One of my favourites in this category is Nutmeg, which kicked off its first year with outstanding success, achieving a ~20% return for investors on its riskiest portfolio over the course of 2013.

I’ve personally used Nutmeg since April 2014, and though I’ve had the usual ups and downs (being down about 5% at one point), I’ve seen peaks of 6-7% in the space of a month.

They have 10 different ‘portfolios’, with 1 being the least risky, and 10 having the most risk (but offering the greatest chance of returns).

I’m on one of their more riskier portfolios, with my funds primarily being invested in the FTSE 100, FTSE 200, and S&P 500. It’s in their best interests for them to generate you the best possible ROI, since they take 1% annually as a fee. This means they’re constantly tweaking your portfolio as the markets change.

During the Scottish independence vote, they sold all UK ETF’s in preference of US equivalents which had been performing similarly.

Nutmeg’s fee structure is fairly simple, taking 1% on a monthly basis.

If you go for this option, you should be able to focus on long-term earnings rather than making a fast return.

5. ‘Execution-only’ investment accounts (investing in individual stocks & shares)

This is probably the option with the most associated risk of the five different ways of earning on your cash I’ve mentioned, but offers the greatest potential for return if you know what you’re doing.

For example, if you’ve been reliably tipped that a particular stock will perform well, and you feel confident enough that you’re willing to invest, this is the option for you.

You’ll be able to log in to an online account, deposit funds, and place an order for a stock of your choosing (listed on the LSE, NYSE etc).

There are many stockbrokers to choose from, though I use x-o.co.uk – mainly down to the fees which consist of a flat £5.95 per trade (buy/sell). Hargreaves Lansdown are another popular option, and though their fees are slightly higher, they have a nicer interface with real-time stock prices. Though their fees could work out to be a substantial percentage for smaller trades, they’re still fairly competitive.

Alternatively, you can trade offline over the counter at your local bank. HSBC charge around £12 I think, with others charging similar rates.

Ideally, a combination of all the above would be a nice spread to give a good return, but also cover any potential losses.

Disclaimer: Okay, so I should probably point out I’m not a financial adviser.

But, that said.. you really shouldn’t just sit on a pile of cash that isn’t doing anything. After all, each year your money is becoming worth less and less due to the growing rate of inflation.